The Story of Underwriting Evolution

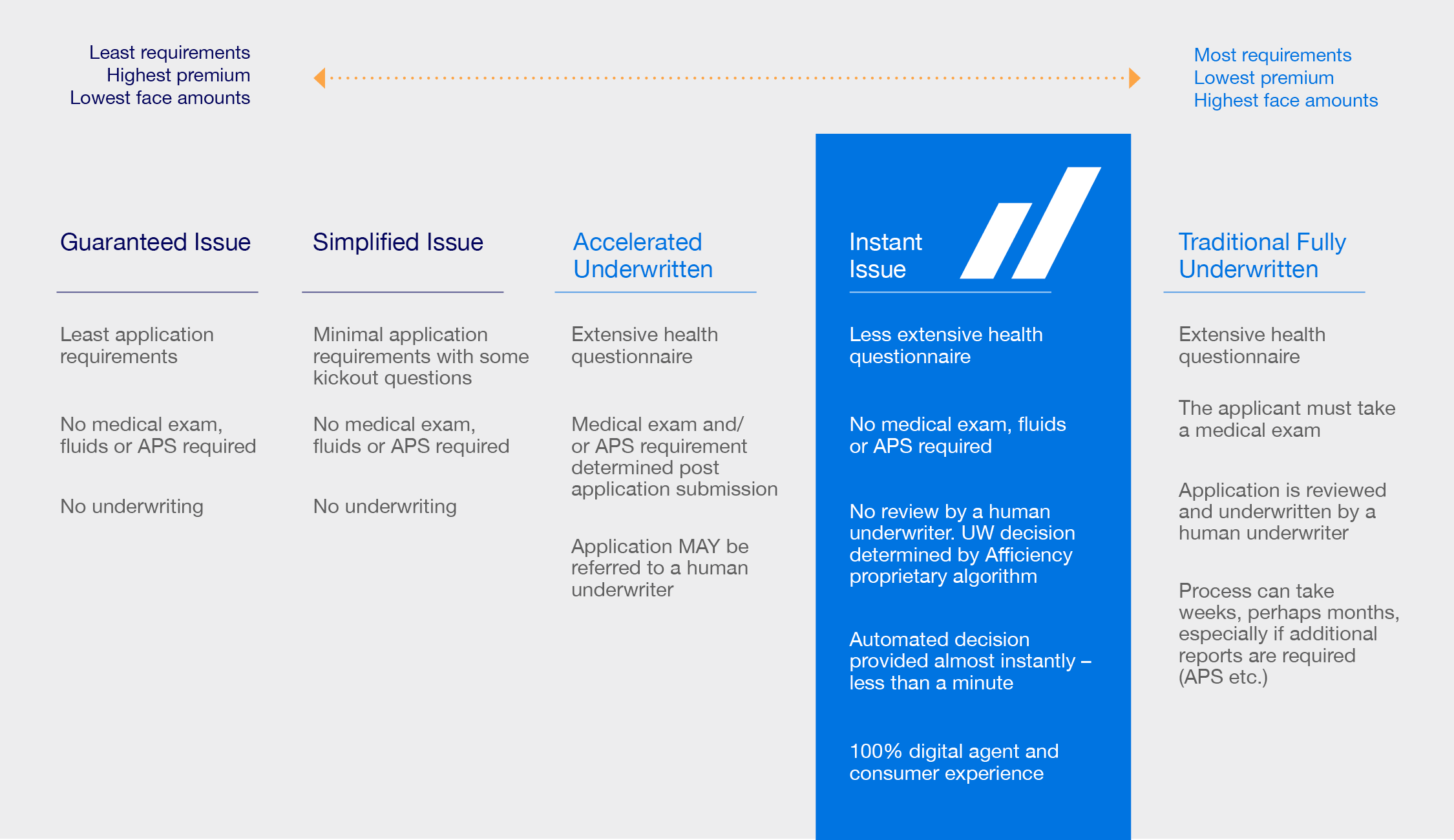

Not so long ago all policies were traditionally underwritten, while this allowed for the lowest premiums and broad face amounts, it also required an extensive health questionnaire, an invasive and time consuming medical exam, Attending Physicians Statement (APS), and often weeks, if not months, of waiting for an underwriting decision. This high-touch,...

Read More

The Story of Underwriting Evolution

Not so long ago all policies were traditionally underwritten, while this allowed for the lowest premiums and broad face amounts, it also required an extensive health questionnaire, an invasive and time consuming medical exam, Attending Physicians Statement (APS), and often weeks, if not months, of waiting for an underwriting decision. This high-touch, time-consuming process was at odds with consumer expectations of obtaining coverage immediately.

At the opposite end of the underwriting spectrum are guaranteed issue products – characterized by zero underwriting, minimal application questions or the need for a medical exam. As a result, guaranteed issue products are limited by lower face values and often have higher premiums.

Coupled beside guaranteed issue life products are simplified issue products – offering slightly higher face values and slightly lower premiums, offset with marginally more application questions. While there can be some applicant knockouts, there is no requirement for a medical exam or extensive underwriting.

Accelerated underwriting has been in vogue for several years; many if not all life carriers now offer a line-up of products that rely more heavily on data and analytics to drive their underwriting decision. However, the consumer may still be required to undergo a medical exam, provide an APS and/or be referred to a human underwriter, more akin to traditional underwriting. As a result, products under the accelerated underwriting umbrella can offer greater face values and lower premiums relative to their simplified and guaranteed issue cousins.

Read Less

{kind=link}